The global transition to instant payment networks has created a critical vulnerability known as Payment Runtime Exposure, which represents the microscopic window of time where a digital transaction is processed and irrevocably settled. Because these real time transactions settle in milliseconds, traditional fraud prevention methods that rely on human review or delayed batch processing are entirely obsolete. Fraud syndicates now leverage automated scripts, artificial intelligence, and sophisticated social engineering to exploit this exact speed. To survive, financial institutions must abandon legacy rules engines and adopt zero latency, AI powered decision platforms that analyze behavioral biometrics and contextual telemetry instantly. This structural shift completely removes the human bottleneck while strictly securing the transaction before the funds clear.

It is 2:14 AM on a holiday weekend in the network operations center of a tier one regional bank. A legitimate corporate client, a logistics firm, has their API credentials compromised via a highly sophisticated supply chain attack. The attackers do not immediately drain the account. They wait for the lowest staffing period. At precisely 2:15 AM, an automated script initiates three hundred simultaneous transfer requests via the newly adopted real time payment rail.

Each transaction is perfectly formatted. Each request is just under the ten thousand dollar automated reporting threshold.

The bank routing systems receive the API calls. The legacy fraud engine looks at the IP address, verifies the session token, and checks the account balance. The logic gates open. In roughly two hundred milliseconds, the transactions are authorized, routed through the central bank clearinghouse, and deposited into three hundred disparate destination accounts across the globe.

A human fraud analyst arrives for the morning shift five hours later. They see a severity one alert generated by an overnight batch process. They lock the compromised account and begin the recall process. The effort is completely futile. The funds have already been layered through cryptocurrency exchanges and dark web mixers.

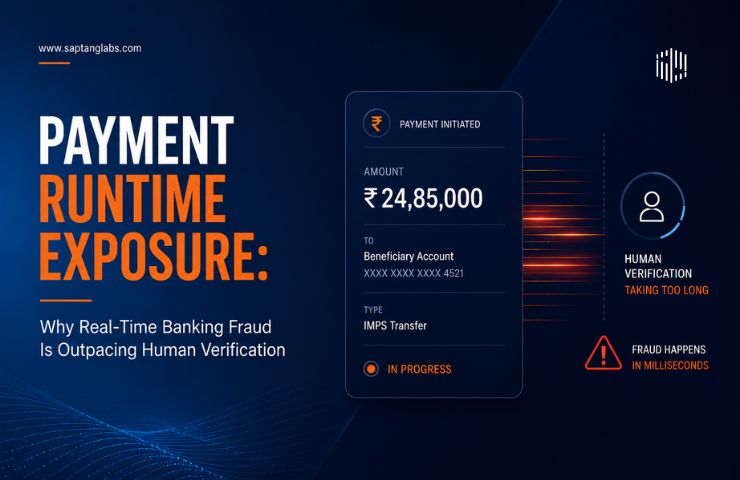

This scenario illustrates the absolute breakdown of traditional financial security. We call this critical failure point Payment Runtime Exposure. As consumer and corporate demand forces banks to adopt instant settlement architecture, the defensive layer has failed to match the velocity of the payment layer. The speed of innovation has completely outstripped the speed of verification.

To understand the severity of this vulnerability, we must look at how digital money movement has evolved. In legacy banking infrastructure, a transaction was essentially a localized promise. When an Automated Clearing House transfer was initiated, the data sat in a pending state. The actual settlement of funds took anywhere from 24 to 72 hours.

That massive window of time was the ultimate security blanket for financial institutions. It allowed risk teams to run complex, heavy analytics across multiple databases. It allowed algorithms to score the transaction at the end of the day. Most importantly, it allowed human beings to review suspicious flags and manually intervene before the money actually left the vault.

Instant payment networks like FedNow, the Clearing House Real Time Payments network, and Europe’s SEPA Instant have permanently erased that security blanket. They mandate that the entire lifecycle of a transaction be completed in seconds. The exposure window has collapsed.

Payment Runtime Exposure occurs during that exact fraction of a second. The system must authenticate the user, check for sufficient funds, screen against global sanctions lists, evaluate the likelihood of fraud, and finalize the transfer. If the system fails to spot an anomaly during this microscopic window, the transaction becomes mathematically irreversible.

Key characteristics defining this modern vulnerability include:

For the last twenty years, the financial sector relied heavily on a hold and review methodology. Risk departments built massive lists of static rules. If a transaction exceeded a certain dollar amount, originated from an unusual geolocation, or triggered a velocity limit, the system would freeze the payment. A ticket would then populate in a queue for a human investigator.

This methodology is fundamentally incompatible with the architecture of instant money movement. Network mandates explicitly prohibit holding these transactions for manual review. The bank must return a binary decision immediately.

When institutions attempt to bolt legacy rules based systems onto instant payment rails, they encounter catastrophic operational failures. Static rules lack nuance. They generate unmanageable volumes of false positives. If a bank automatically declines every transaction that looks slightly unusual, they will aggressively block legitimate customer payments. This creates severe reputational damage, drives customer churn, and forces executives to manually override security protocols just to keep business moving.

The core reasons traditional controls fail in real time:

The acceleration of payment networks has driven a massive shift in criminal methodology. Instead of spending months trying to breach hardened banking mainframes, attackers now target the softest element in the security chain. They target the human beings who hold the legitimate account credentials.

This strategic pivot has led to an explosion in Authorized Push Payment fraud. In an Authorized Push Payment scenario, the victim is fully authenticated. They log into their own banking portal from their own registered device. They use their own biometric face scan. They then willingly initiate an instant transfer directly to a fraudster.

The victim believes they are paying a legitimate supplier invoice, helping a desperate family member, or making a lucrative cryptocurrency investment. Because the legitimate user initiates the payment, traditional account takeover defenses remain completely silent. The IP address matches historical data. The device fingerprint is recognized. The password is correct. From a purely technical standpoint, the transaction looks completely flawless during the runtime exposure window.

Primary vectors driving this specific fraud trend include:

To successfully secure the Payment Runtime Exposure window, the financial sector must completely remove the human bottleneck from the initial decision making sequence. The only technology capable of analyzing vast datasets and rendering highly accurate decisions within a fifty millisecond timeframe is advanced artificial intelligence.

Modern AI fraud detection platforms do not rely on simple static rules. Instead, they utilize complex machine learning models that continuously analyze user behavior. These models establish a highly detailed baseline of normality for every individual customer and entity.

Consider a corporate treasury manager initiating a large transfer. An AI system looks far beyond the correct password. It analyzes the typing cadence. It detects if the mouse movements are erratic or rushed compared to the historical baseline. It cross references the destination account against global threat intelligence feeds. It recognizes if the user is currently on an active voice call, which is a massive indicator of an active social engineering scam.

The AI evaluates thousands of these contextual data points simultaneously. It calculates a precise risk score and forcefully blocks the transaction before the funds ever leave the core banking system.

Core architectural components of AI driven defense:

Transitioning from a reactive, human dependent fraud team to an autonomous, AI driven security posture requires a fundamental architectural overhaul within the enterprise. Organizations must aggressively dismantle internal data silos. The card fraud team, the wire operations team, and the digital banking team can no longer operate in isolation.

A zero latency security posture demands a unified data integration layer. This layer must ingest telemetry from every possible customer touchpoint. When a user logs into the mobile application, speaks with the call center, and makes a web purchase, all of this context must feed into a single, centralized decision engine in real time.

If a fraudster tests a stolen identity with a small digital wallet purchase, the system must instantly apply that risk intelligence to the customer’s primary checking account. This prevents any subsequent attempts to initiate an instant bank transfer.

Strategic steps to build this resilient infrastructure:

The escalating crisis of real time banking fraud has forced global regulators to take unprecedented action. Historically, financial institutions generally held the customer fully responsible if the customer willingly authorized a push payment to a scammer. The legal logic was straightforward. The bank processed the request exactly as instructed.

That paradigm is currently undergoing a massive reversal. Regulators in the United Kingdom, the European Union, and increasingly in the United States are heavily modifying liability frameworks.

New regulations are forcing banks to completely reimburse victims of Authorized Push Payment fraud. This fundamentally alters the financial calculus for institutions. When the bank is forced to cover the massive losses of every customer tricked by a sophisticated scam, investing in ultra low latency fraud detection stops being a mere compliance exercise. It becomes a critical survival imperative. The cost of failing to secure the Payment Runtime Exposure window is now directly hitting the institution’s bottom line.

The path forward requires total alignment between security architecture and business operations. Banks must educate their customers with highly targeted, in journey warnings that appear exactly when a user attempts a high risk transfer. They must collaborate closely with telecommunications providers to intercept spoofed text messages and fraudulent phone calls before they ever reach the consumer. Most importantly, they must fully embrace autonomous decision engines that operate at the exact same speed as the instant payment rails they are trying to protect.

What exactly is Payment Runtime Exposure?

It is the extremely brief period of time, usually measured in milliseconds, during which a digital transaction is processed, authorized, and finalized. Because modern banking systems settle funds instantly, security infrastructure has almost no time to analyze the transaction for fraud before the money is irrevocably transferred.

Why cannot human analysts review instant payments for fraud?

Instant payment networks strictly mandate that transactions settle in seconds. A human analyst needs several minutes to open a file, review the context, check external databases, and make a confident decision. By the time a human even opens a security alert, the funds have already left the bank and bounced through multiple offshore intermediary accounts.

What is Authorized Push Payment fraud?

This occurs when a fraudster uses advanced social engineering, such as posing as a trusted vendor or a government official, to trick a victim into willingly sending them money. Because the legitimate account owner is the one logging in and authorizing the transfer, traditional security measures like passwords and device checks do not flag the activity as malicious.

How does artificial intelligence stop fraud in real time?

AI systems utilize complex machine learning models to analyze thousands of data points simultaneously, including behavioral biometrics, geolocation, transaction history, and network metadata. These systems establish a baseline of normal behavior for every user and can instantly detect anomalies, blocking suspicious transactions in milliseconds without any manual human intervention.

Will entirely replacing human verification with AI cause legitimate transactions to be blocked?

If configured poorly, yes. However, modern AI systems use a concept called adaptive friction. Instead of blindly blocking a payment that looks slightly unusual, the system instantly prompts the user for additional verification, such as a biometric facial scan or answering a context specific question. This allows legitimate payments to proceed safely while stopping automated attacks.

Who is legally responsible when a customer is scammed into making an instant payment?

Historically, the customer bore total liability for authorized payments. However, global regulations are rapidly changing. Many jurisdictions are now forcing the sending and receiving banks to split the cost of reimbursing victims of scams. This places immense financial pressure on institutions to stop the fraud before the transaction clears.

How can a business protect itself against Payment Runtime Exposure?

Businesses should implement rigorous internal payment controls, such as requiring dual authorization for all large outbound transfers. They must conduct continuous employee training to recognize phishing and sophisticated social engineering tactics. Furthermore, they should rigorously ensure their financial partners utilize state of the art, real time AI monitoring systems that scrutinize every transaction simultaneously.

You may also find this helpful insight: Adaptive Threat Orchestration: Why AI-Driven Intrusions Are Breaking Traditional Detection Timelines